Are we on the right road to the energy transition?

Summary

To date, efforts on energy transition have been characterized by an “all of the above” approach, with a wide range of feedstocks and technologies seeking to decarbonize a wide range of different fossil fuel end-uses.

This approach is hampered mainly by insufficient renewable power, insufficient biomass feedstock, high costs for many “end-use” technologies and lack of infrastructure for new fuels.

This is leading to inefficient distribution of resources (finance, time and biomass, i.e. carbon) among numerous routes, not all of which are even viable.

The most efficient way to reduce emissions overall is to supplement renewable power and unavoidable biofuels (SAF etc) by using the most widely available feedstock (cellulosic biomass) via the lowest cost technology (biogas to biomethane) with the widest range of end-uses (CNG, LNG, heat, power etc).

In this way, resources and effort can be concentrated and focused on the point of maximum impact.

The energy transition is hampered by 10 key factors

More than ten years after the landmark Paris Agreement, progress on the goal of net zero emissions by 2050 is far from on track. The energy transition is being stymied by 10 key factors:

Shortage of Renewable Mass / Molecules: Simply put, we are short on available carbon with which the fossil-derived carbon used in both fuels and chemicals can be replaced. The key potential sources are biomass and captured carbon, both of which face significant scale challenges.

Shortage of Low Carbon Intensity (CI) Electrons / Energy: Just as we are short on available carbon molecules, we are also short on available power. Power consumption is increasing, particularly as electrification becomes a viable option for decarbonization, and other uses - mainly for AI and data centers – are growing at extraordinary rates. This rapid growth risks offsetting the admittedly very high growth of solar, wind, nuclear and other zero carbon power capacity, and diminishing their ability to erode demand for the highest emitting fossil energy source, coal. While its use is plateauing, coal still accounted for over 30 percent of global power generation in 2025.

Shortage of “Steel in the Ground”: While significant efforts have been made to develop sustainable alternatives, meaningful replacement of fossil fuels by 2050 would require building rates exceeding those of the industrial revolution on several fronts; this is highly unlikely to actually occur.

Diversity of Replacement Strategies: Given the multiplicity of end-uses for fossil-derived products, efforts to replace them in individual applications have led to a proliferation of different solutions, all requiring high levels of investment; notably, most biofuels aim to replace a single product (e.g,. ethanol for gasoline/petrol) and are limited by blend rates.

Shortage of “Easy” Low CI Bio Feedstocks: While some biofuel feedstocks benefit from low Carbon Intensity and relative ease of use (notably Used Cooking Oil and tallow for Sustainable Aviation Fuel and Renewable Diesel) supply of these is severely constrained relative to the potential needs of a decarbonizing transport market.

Technical Barriers for “Hard” Low CI Bio Feedstocks: On the other hand, while other low CI feedstocks – chiefly cellulosic biomass – are theoretically widely available, many of the technical routes to their use (cellulosic ethanol, biomass gasification etc) have been slow to proliferate, facing commercialization problems and high costs.

High Cost of Other Low CI Options: Other very low Carbon Intensity alternatives are emerging, notably Power-to-Liquids (PTL/e-fuels) processes; however, these come at a very high cost and (as noted above) are dependent on the availability of renewable power.

High Cost of Direct Air Carbon Capture: DAC has been the focus of significant attention, both as a direct mitigant of emissions and as a source of captured CO2 necessary for e-fuels production; however, while technically feasible, costs are extremely high, typically due to very high capital costs and energy requirements.

CCUS is Slow and Not for All Applications: Carbon Capture, Utilisation and Storage (CCUS) is growing slowly, is generally only best for high concentration CO2 sources (e.g., hydrogen production) and is mostly in use for Enhanced Oil Recovery, which can be viewed as counterproductive at best.

Infrastructure and Logistics Matters: Many fossil end-uses have significant sunken capital and infrastructure. For example, aviation has airport infrastructure, aircraft lifetimes (measured in decades) and costs, infrastructure costs, logistics, and energy density among other considerations required to decarbonize. Drop-in fuel applications will accordingly be favoured for these applications.

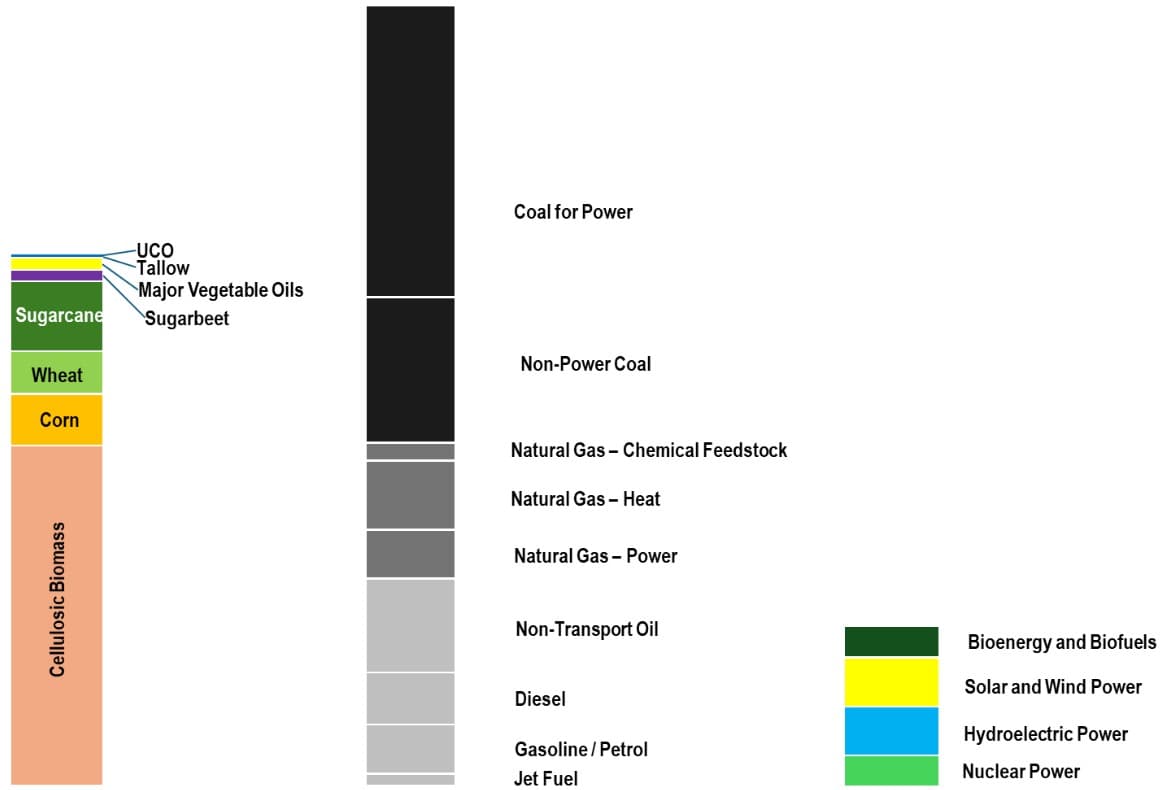

Underlying these individual challenges is the sheer scale of the task; comparing estimated 2025 fossil fuel consumption with the sum of 2025 potential alternatives (not even accounting for other uses of these alternatives such as food) illustrates this challenge:

Relative Supply of Major Biofeedstocks vs Fossil Fuel Consumption vs Low CI Energy

Mass Basis and MTOE, 2025

Image Source: FGE NexantECA Analysis

Power generation: Even with rapid growth, renewables are challenged to keep pace with rising demand

One part of the challenge – the lack of low/zero carbon power – is of course addressed by the continuing sharp growth of solar, wind and other renewable generation capacity, alongside growing nuclear capacity. Renewables are estimated to have surpassed coal in terms of their share of global power generation in 2025, but coal still accounted for 34 percent of total generation, with natural gas taking a further 22 percent. Despite the rapid growth of solar and wind power, renewables still face a major challenge in the power sector. Notably, growth risks being offset by rapidly increasing demand from data-driven applications (data centres, AI etc) and the ongoing electrification of various fossil end-uses (including road transport), potentially slowing the decline of coal-fired generation. Accordingly, any additional source of low/zero carbon power – including from biomass – will be a welcome addition.

Other end-uses: Biomass feedstocks will be required, despite emerging alternatives

Clearly, there are multiple pathways to decarbonising the range of non-power end-uses for fossil fuels for uses such as transport, heat, chemical production and industrial use. Electrification remains a key option (“electrify everything”) but meaningful emissions reduction requires extensive additional renewable power capacity (already challenged, as above, to displace coal from current power use). Many end-uses are also subject to the infrastructure and logistics issues noted above, meaning that alternative routes to the products currently derived from fossil fuels (i.e. substitute carbon atoms) will continue to be required.

Several emerging low CI technologies offer the prospect of fuels from sources other than biomass, or from new forms of biomass. Most notably, e-fuels processes are progressing rapidly (spurred by incentivised demand in the European aviation sector and likely demand from the shipping industry). However, e-fuels are also dependent on sufficient availability of renewable power capacity, have extremely high production costs, and are unlikely to find markets beyond those “hard to abate” sectors (aviation and shipping) where their use is likely to be encouraged.

Elsewhere algae-based technologies have experienced several waves of attempted commercialization with little success, and are dogged by excessive costs, while the mitigation of emissions via Direct Air Capture is still undergoing commercialization, with costs also expected to be excessive. Accordingly, biomass feedstocks will need to continue to play a significant role in overall decarbonisation.

Easy to use low CI biofeedstocks are supply constrained, while more widely available feedstocks are hampered by technical and cost barriers

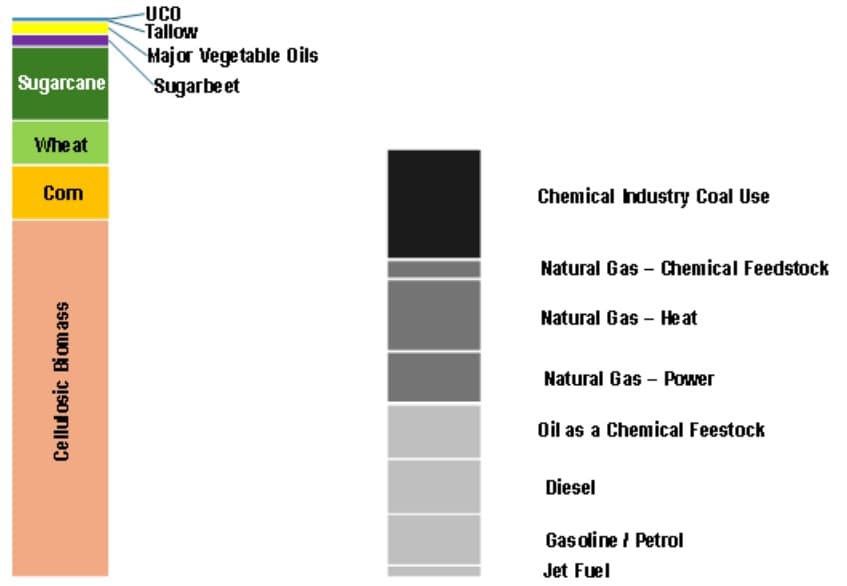

However, comparing the “addressable” share of total fossil fuels consumption – i.e. excluding power generation – with the estimated availability of the most widely available biomass feedstocks, as shown below, shows that the most widely used biofuels at present – ethanol and methyl ester biodiesel from crop-based feedstocks – face their own challenges, around overall Carbon Intensity, food competition, sustainability, and maximum blending levels. Notably, even were the entire supply of corn, wheat, sugarcane and vegetable oils to be used for fuel (clearly impossible given their primary roles in food), they would not come close to equalling the scale of the challenge.

Relative Supply of Major Biofeedstocks vs Addressable Fossil Fuel Consumption

Mass Basis, 2025

Image Source: FGE NexantECA Analysis

The problem is exacerbated by the fact that biofeedstocks are not as carbon rich as their fossil fuel counterparts. Cellulosic biomass, corn, wheat, sugarcane, and sugar beet have significant heteroatom (particularly oxygen) content. For fermentations (e.g. ethanol), this is usually removed at a cost of half of the carbon. Furthermore, the masses shown are for the entire corn kernel and/or sugarcane stalk, which are not entirely sugar/starch. While natural oil feedstocks are significantly more carbon rich, their relative supply remains very small. Waste oils such as Used Cooking Oil and tallow have low CI but their long-term availability is constrained, as they cannot easily grow beyond improvements in collection.

In fact, the only biogenic source of carbon atoms available at near the required scale is cellulosic biomass, including agricultural residues, forestry waste and municipal solid waste. There have been several pushes to commercialize advanced cellulosic technologies, mostly via ethanol, dating back to the late 1900s as well as multiple attempts in the last 20 years. However, these have been met with limited success, and little to no proliferation, with examples including:

Many failed attempts at cellulosic hydrolysis and fermentation to ethanol, with a few limited successes (e.g. in Brazil)

Many failed attempts at cellulosic sugars production

Failed attempts at biomass gasification to ethanol (e.g. Range Fuels)

Non-proliferation of biomass gasification to methanol (e.g. Enerkem)

Failed attempts at biomass gasification to Fischer Tropsch liquids (e.g. Fulcrum, Solena)

Biomethane is the lowest cost, most technically feasible route to using cellulosic and other waste biomass

While these commercialisation efforts have been going on, biomethane – methane purified from biogas produced from biogenic sources – has grown steadily, and is emerging as a major potential decarbonisation option, both for power and non-power use. Biomethane’s precursor, biogas (methane diluted by CO2, H2O, and other contaminants) is produced from a range of sources, including agricultural waste (residues, animal manure etc), municipal waste/landfill waste, and wastewater treatment/sewage. The main production processes are anaerobic digestion and landfill capture. Anaerobic digestion and landfill gas capture technologies are relatively simple in principle but have been rigorously developed to be as efficient as possible. Carbon Intensity is low compared to fossil natural gas (and extremely low in some cases such as animal manure) dependent of the volume of methane that the waste stream would otherwise have emitted, as shown below.

Example: Carbon Intensity – Fossil Gas & Biomethane

(NexantECA Estimates of representative CI range)

Image Source: Market Insights: Biomethane (2023)

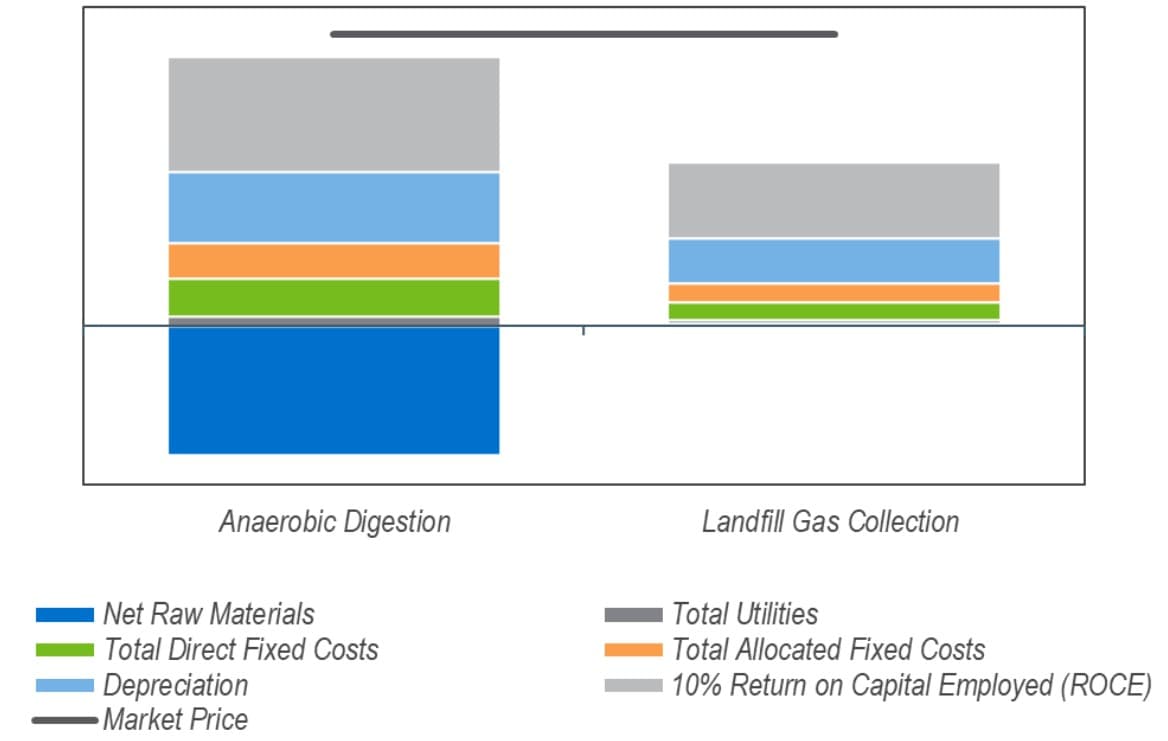

In addition, biomethane can be produced competitively with fossil natural gas, as shown below.

Example: Biomethane Economic Competitiveness in Western Europe

(Q3 2025)

Image Source: Biorenewable Insights: Biomethane (2025)

Currently, biogas is most often used to generate heat or electricity via commercially proven combined heat and power (CHP) plants. Anaerobic digestion and landfill gas collection plants commonly use some of their generated biogas to provide both heat and power. However, when upgraded to pure biomethane, the following end-uses can be addressed:

Space heating

Cooking fuel

Fuel for internal combustion engine vehicles (e.g. as road CNG or marine LNG)

Fuel cell-electric vehicle fuel

Industrial motive power (LNG and CNG)

Steam generation

Chemical feedstock (e.g. hydrogen, ammonia, methanol, etc)

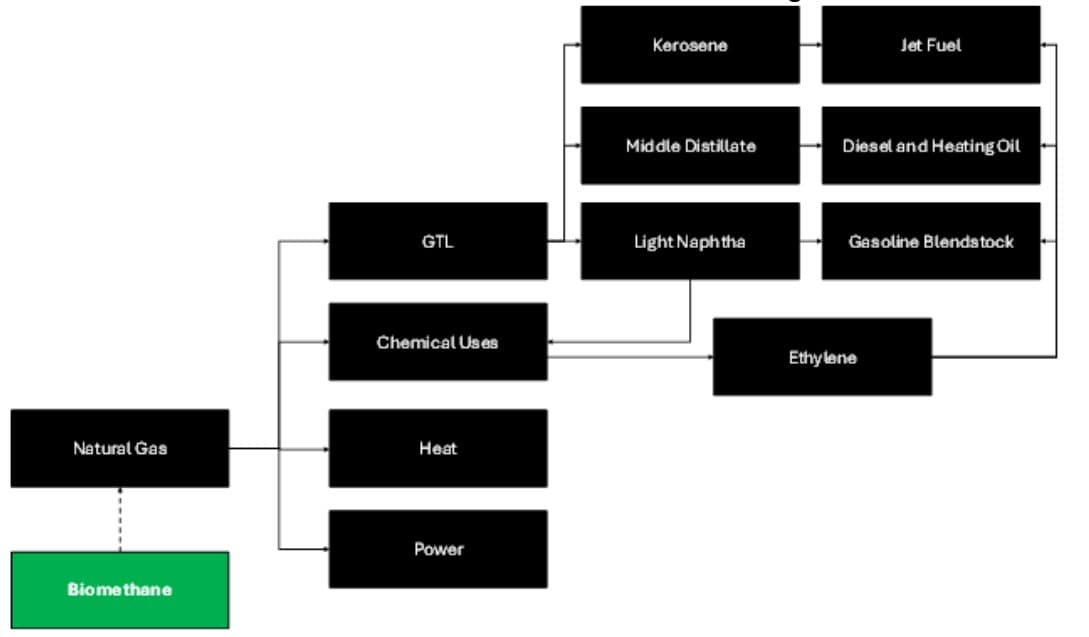

Biomethane is also fungible with natural gas, and as such is a drop-in to the existing value chain. This helps with the “steel in the ground problem”. Additionally, using only commercial technologies for natural gas, biomethane may be converted into many of the end uses shown previously in the addressable markets.

The integration of current sources of biomethane such as landfill and agricultural biomass digestion into the current natural gas ecosystem can not only provide economic benefits to landfill owners and waste generators, but to the end-consumers of energy and communities without access to sufficient energy at reasonable cost. This, coupled with the potential to reduce emissions relative to current systems, makes the prospect of a biomethane energy economy an attractive possibility.

Currently unharnessed sources of low carbon biomethane can be directly substituted for natural gas, taking advantage of existing distribution infrastructure and assets. The use of biomethane directly in gas-fired electric power generation goes beyond mere substitution and direct reduction of emissions; due to the well-known ability of gas-fired power plants to act as rapidly deployable reserves, the use of biomethane with such facilities can improve grid reliability by acting against drops in grid voltage stemming from heavy use of intermittent renewable power in the distribution systems of the future.

Natural Gas and Biomethane Value Chain Technologies

Image Source: FGE NexantECA

At present, Europe is the largest biomethane-producing region. Asia Pacific, which accounts for around 10 percent of global production, is expected to grow rapidly. South America, the Middle East, and Africa are small biogas producers with little production growth expected. Biomethane production globally is minimal compared to existing natural gas production and consumption, meaning that significantly larger volumes of biogas will have to be produced to have any impact on global natural gas markets and broader fossil fuel markets. In the United States, high adoption rates of biomethane from landfill gas have already been seen, and over 60 percent of candidate landfills are already undergoing some sort of landfill gas project. In other regions, adoption rates are much lower.

Using natural gas to displace coal and oil paves the way for biomethane scale-up

In the short-term, the growth of biomethane resources obviously still present a major challenge. However, even fossil natural gas, if leaks are mitigated, has the potential to be a much cleaner source of power than coal or oil, while supplying most of the same markets. A reasonable energy transition could include natural gas as a transitional fuel/feedstock, until such time as markets are no longer short on the molecules and electrons needed to fully displace fossil fuels, avoiding the risk of resurgent coal use as energy demand rises. Natural gas can be a powerful ally to remove coal and crude oil from the energy equation. Once that is accomplished, natural gas can itself be displaced, and with the energy value chain already set to work on natural gas, biomethane, which is the only proliferated cellulosic biofuel/feedstock, can drop directly into the value chain. While natural gas is certainly not a “net zero” fuel or feedstock, it is “lower than the average” which is still a step in the right direction, and one that paves the way for biomethane – a real contributor to meaningful decarbonisation – to step in.

About Us - FGE NexantECA is the leading advisor to the energy, refining, and chemical industries. Our clientele ranges from major oil and chemical companies, governments, investors, and financial institutions to regulators, development agencies, and law firms. Using a combination of business and technical expertise, with deep and broad understanding of markets, technologies, and economics, FGE NexantECA provides solutions that our clients have relied upon for over 50 years.

Contact a member of our team to see how we can support your operational, investment, or trading decisions