Hydroprocessed esters and fatty acids (HEFA) products: Reliability balanced against increasing challenges

Hydroprocessed Esters and Fatty Acids (HEFA) products: Reliability balanced against increasing challenges

As the global push towards “Net-Zero” accelerates, governments and industry stakeholders are actively supporting the development and adoption of renewable fuels to reduce reliance on petroleum-derived fuels.

Among the various emerging renewable fuels technologies, hydroprocessed esters and fatty acids (HEFA) represents the most commercially advanced pathway, with over 70 facilities currently operating globally – comprising of standalone plants, converted refineries and co-processing units within petroleum refineries.

The rising interest in HEFA Products is driven by several key advantages:

GHG reductions: HEFA products, particularly HEFA renewable diesel (RD), which accounts for about 90 percent of total demand – offer immediate greenhouse gas (GHG) emission reductions, without the blend wall limitations seen in first-generation biofuels like FAME biodiesel and ethanol.

Drop-in compatibility: These products are fully fungible, meaning that they are compatible with existing engines and fuel infrastructure, allowing for seamless integration into sectors such as road transport, aviation, petrochemicals, etc. Specifically, HEFA sustainable aviation fuel (SAF) is currently approved under ASTM standards for up to 50 percent blending with conventional jet fuel, underscoring its technical readiness.

The HEFA pathway converts a broad range of lipid-based feedstocks – rich in fatty acids and triglycerides – into a range of renewable fuels with diverse end-uses. While HEFA is predominantly used for the production of RD, there is a growing shift towards SAF, given the aviation sector’s classification as a hard-to-abate industry. The process also yields by-products such as renewable naphtha (RN) and renewable LPG (RLPG); however, in the absence of specific regulatory incentives, demand for these co-products remains comparatively limited.

HEFA value chain

HEFA products demand is estimated to reach around 20 million tons per year in 2025, with strong CAGR projected through to 2040. While HEFA RD currently dominates in absolute demand, HEFA SAF is poised to become the primary growth driver, supported mainly by increasing airline adoption and regulatory mandates targeting emissions reduction. In contrast, co-products such as HEFA RN and HEFA RLPG are often recycled within HEFA facilities, either as hydrogen feedstock or process fuel, to lower the overall carbon intensity (CI) of production, reflecting limited current market incentives for external sales. However, the outlook for these co-products may improve as policy frameworks broaden to support low-carbon petrochemicals and sustainable domestic heating, opening new avenues for market growth.

HEFA’s feedstock flexibility to process a wide range of feedstocks – including waste and residues such as used cooking oil (UCO), palm oil mill effluent (POME) oil and inedible animal fats – has been central to its success so far. However, future capacity expansions are expected to face mounting feedstock constraints, especially as producers transition towards waste-based options.

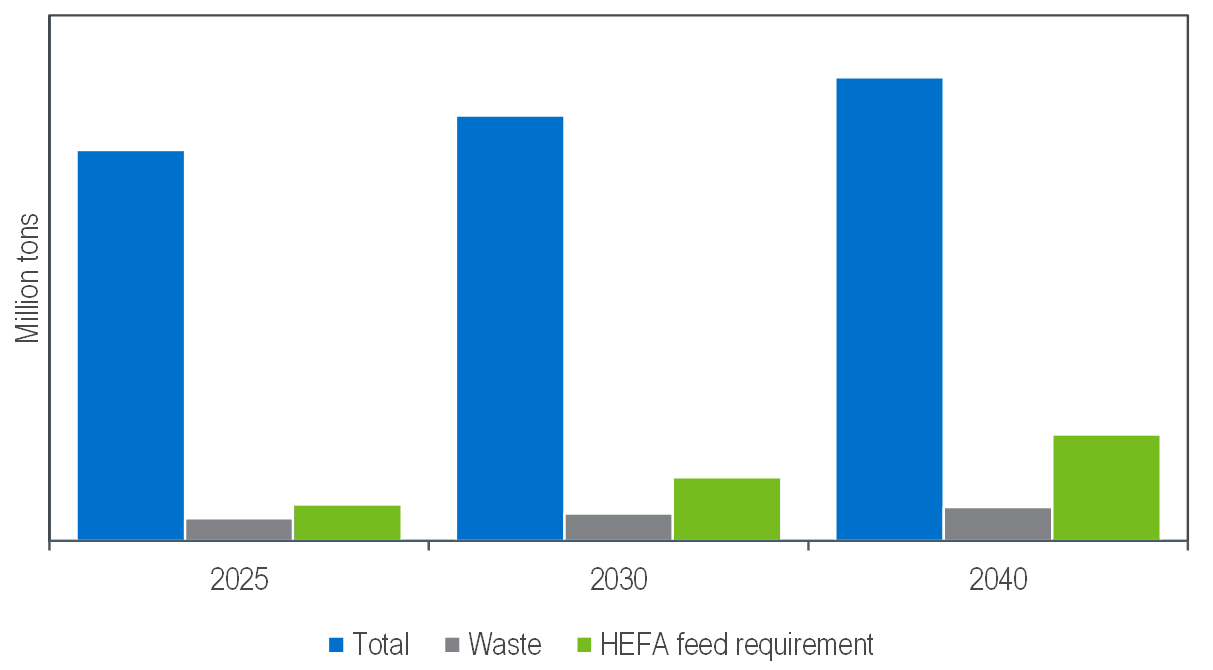

Early HEFA adopters relied heavily on first-generation feedstocks, but this is changing rapidly due to tightening policy restrictions and sustainability caps, especially in key demand centres such as Western Europe. For instance, the ReFuelEU aviation regulation explicitly excludes palm-based feedstocks (with the exception of POME oil and empty fruit bunch (EFB oil), placing greater pressure on the limited global supply of waste-based feedstocks like UCO and POME oil—both of which are unlikely to scale fast enough to match projected HEFA capacity growth, as illustrated in Figure 1.

In North America, the regulatory approach appears to be more feedstock-neutral, with fewer restrictions on first-generation inputs, although some states have explicitly excluded the eligibility of selected feedstocks (e.g. palm-based) from qualifying for tax credits. Nevertheless, most HEFA producers increasingly prioritise waste-based feedstocks to maximise credit generation under carbon intensity (CI)-based incentive schemes, as these feedstocks typically offer more favourable CI scores.

In other regions, particularly those with a structural surplus of vegetable oils, the use of first-generation feedstocks may remain economically and logistically viable, depending on the local policy environment and biofuel production economics. However, this is unlikely to apply to SAF production, as most jurisdictions—especially those with established SAF mandates—exclude or discourage the use of first-generation vegetable oils for aviation use due to sustainability concerns and international policy alignment.

Figure 1 Global HEFA Feedstock Availability

Future of HEFA Products

The HEFA producer base was initially led by a small group of early adopters, but is now becoming increasingly fragmented as more players enter the market. However, feedstock constraints—especially around high-demand waste oils like UCO—pose a significant challenge to further scaling. As demand for waste-based inputs intensifies globally, sourcing sustainably certified, low-carbon feedstocks like UCO and POME oil is becoming increasingly competitive and geographically constrained. To mitigate long-term supply risks and promote the development of emerging SAF pathways, governments are beginning to place caps on HEFA-derived SAF. For example, the UK has introduced a HEFA cap under its SAF mandate to steer investments toward advanced technologies with greater decarbonisation potential and feedstock diversity (notably the Power-to-Liquids, or e-fuels, route).

A further challenge is the relative slowness of non-mandated SAF markets (i.e. most regions other than Western Europe) to increase consumption. While numerous non-EU/UK markets have floated mandate plans, few are as yet being implemented, resulting in a heavily concentrated end-use market, and even a degree of overcapacity in the short-to-medium term.

Despite these policy signals and growing concerns around feedstock availability, HEFA is still projected to play a major role in renewable fuels production over the coming decades, particularly in the near to medium term as alternative pathways mature.

Find out more…

NexantECA’s Market Insights: Hydroprocessed Esters and Fatty Acids (HEFA) Products – 2025 provides detailed forecasts to 2040 for global supply, demand and trade of HEFA Products, including HEFA RD, HEFA SAF, HEFA RN and HEFA RLPG. It examines key market drivers, policy developments and constraints impacting growth of these products across regions. The report also includes detailed feedstock analysis as well as pricing trends and margin analysis by product. The Executive Summary is available separately to subscribers.

About Us - FGE NexantECA is the leading advisor to the energy, refining, and chemical industries. Our clientele ranges from major oil and chemical companies, governments, investors, and financial institutions to regulators, development agencies, and law firms. Using a combination of business and technical expertise, with deep and broad understanding of markets, technologies, and economics, FGE NexantECA provides solutions that our clients have relied upon for over 50 years.

Contact our team of industry experts