The low-carbon barrel: How policy is powering profits by gasifying waste into fuel

Every two minutes, the world discards enough trash to fill 1,000 garbage trucks. Over a year, that adds up to 2.1 billion tons—enough to circle the Earth twenty-four times if parked bumper-to-bumper. Most of it ends up in landfills or open dumps responsible for roughly five percent of global greenhouse-gas emissions, where decomposition releases methane and carbon dioxide.

Yet alongside this mounting waste crisis lies an even greater carbon opportunity. Each year, the world generates more than 4.6 billion tons of biomass residues—including crop stalks and husks, forestry offcuts, sawdust, bark, and pulp-and-paper by-products. Collectively, these materials form a vast pool of biogenic carbon—a renewable resource large enough to encircle the planet more than fifty times if hauled by truck.

All of this is unfolding as the planet’s remaining carbon budget consistent with limiting warming to 1.5 °C contracts rapidly from roughly 500 billion tons of CO₂ in 2021 to about 275 billion tons in 2024, leaving only six years of emissions at today’s pace. Meanwhile, global waste generation is projected to rise by 60–80 percent by 2050, driven by population growth and rising consumption in developing economies, while global recycling rates remain stubbornly below 10 percent.

Otay Landfill in Chula Vista, California

Image source: Andri Tambunan/The New York Times/Redux

These converging pressures—rising waste volumes above ground and a shrinking carbon budget overhead—make biomass gasification one of the few scalable technologies capable of reducing waste-related emissions while supplying low-carbon building blocks for fuels and chemicals.

Molecules Matter

Biomass gasification provides low-carbon fuels and chemicals for decarbonization of multiple sectors by converting biogenic carbon—stored in residues, wastes, and other organic matter—into synthesis gas (syngas), a mixture of carbon monoxide and hydrogen produced at temperatures above 1,000 °C. From this molecular foundation, producers can synthesize sustainable aviation fuel, methanol, hydrogen, synthetic natural gas, or generate heat and power for local grids.

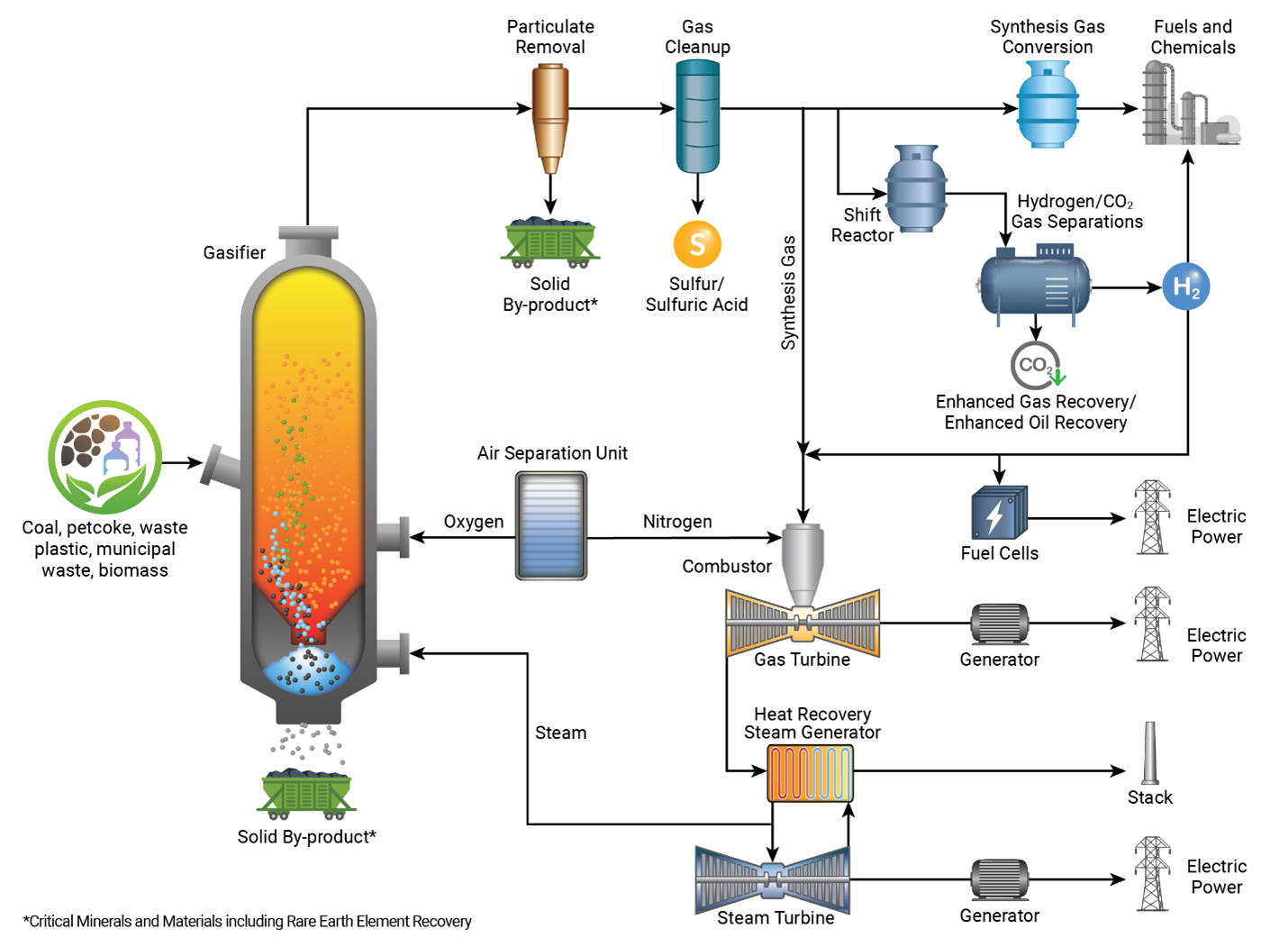

Figure 1 Biomass Gasification Process Flow-Diagram

Source: National Energy Technology Laboratory

Figure 1 above shows how diverse organic feedstocks—agricultural residues, forestry waste, and municipal solid waste—are converted into syngas, a versatile intermediate that can be upgraded into renewable fuels, hydrogen, electricity, or low-carbon chemicals.

Carbon Policy as Profit Engine

Governments are moving decisively to close the loop on both waste and carbon. In the European Union, the Fit-for-55 package mandates a 55 percent emissions reduction by 2030 and a ReFuelEU Aviation target of 70 percent SAF blending by 2050. Verified biogenic CO₂ is treated as zero-emission under the EU ETS, giving captured carbon a tradable value, while new restrictions on plastic-waste exports keep more recyclable carbon within Europe.

In the United States, as of 2025, federal policy continues to reward low-carbon fuel production under the Inflation Reduction Act. Producers can earn up to $1.75 per gallon under Section 45Z, $3 per kilogram under Section 45V for clean hydrogen (for projects beginning construction before 2028), and $85 per ton under Section 45Q for CO₂ stored underground. Combined with the Renewable Fuel Standard (RFS) and California’s Low Carbon Fuel Standard (LCFS), total SAF incentives can exceed $4–5 per gallon, often eliminating the cost gap with fossil jet fuel.

Elsewhere, similar carbon-performance incentives are taking hold. Canada’s Clean Fuel Regulations issue tradable credits for verified lifecycle-emission reductions. Brazil’s RenovaBio converts avoided emissions into CBIO credits, and the Fuel of the Future law sets a national SAF target rising from 1 percent in 2027 to 10 percent by 2037. Japan targets 10 percent SAF by 2030, while Singapore has raised its carbon tax to $19 per ton CO₂e and plans to increase it to between $37–60 USD per ton by 2030, alongside new bunkering standards for methanol and ammonia to decarbonize shipping. China is expanding its national carbon market beyond the power sector to include steel and cement, advancing low-carbon hydrogen and synthetic-fuel programs, and tightening restrictions on open crop-residue burning to channel biomass into energy production.

Technician Refueling aircraft with Sustainable Aviation Fuel (SAF)

TotalEnergies is a partner in the BioTfueL® project, which seeks to convert lignocellulosic biomass into biofuels via gasification, purification, and synthesis chains. Demonstration units for gasification, syngas purification, and Fischer-Tropsch synthesis were built at a site near Dunkirk, adjacent to Total’s Flanders facility.

From Local Heat to Global Fuel

Across Europe and Asia, the backbone of biomass gasification today lies in community-scale combined-heat-and-power (CHP) systems—compact plants that turn local waste into local energy. A typical unit processing 15,000–25,000 tons of feedstock per year costs around $20–30 million and produces 25–40 GWh of substitute natural gas (SNG) or syngas annually, plus surplus heat for district networks. Additional revenue from biochar, liquefied CO₂, and tipping fees—payments from waste suppliers—support project economics. By targeting SNG prices near €150/MWh, many systems achieve payback within five to eight years.

What began as a network of small CHP systems is evolving into a global renewable-fuels platform, turning low-value residues into hydrogen, methanol, and synthetic liquids capable of decarbonizing aviation, shipping, and heavy industry alike.

In China, Shanghai Electric’s Taonan plant is producing 50,000 tons per year of green methanol, expanding to 250,000 tons by 2027, while Inner Mongolia’s Hinggan League project will add another 250,000 tons per year using wind-powered hydrogen and Clariant’s MegaMax™ catalyst.

In Europe, the BioTfueL® program has demonstrated the complete pathway from woody biomass gasification to Fischer–Tropsch fuels, paving the way for SAF and renewable diesel. Meanwhile, Velocys’s Altalto plant in the UK will produce 23,000 tons of SAF per year by 2030. In Spain Repsol–Enerkem’s Ecoplanta project is set to convert 400,000 tons of municipal solid waste into 240,000 tons of renewable methanol by 2029.

The Path Forward

Even if every car ran on electricity and every grid drew solely from renewables, the energy transition would remain incomplete. The hardest-to-decarbonize sectors—aviation, shipping, fertilizers, and petrochemicals—depend not only on electrons, but on carbon molecules.

The challenge is not to eliminate carbon, but to replace fossil carbon drawn from geologic reservoirs with renewable carbon already circulating in the biosphere. Because the CO₂ released during combustion was first absorbed from the atmosphere, biogenic carbon recirculates through rather than adds to the global total—a principle that underpins all advanced biofuels.

The technical barriers of gasification have evolved. The test is no longer just tar cracking or ash control, but reliability and uptime. Facilities that secure diverse feedstock contracts, maintain <3 % ash and <10 % moisture, and sustain >90 % availability are now setting the new benchmark for commercial success.

In FGE NexantECA’s latest techno-economic modeling, biomass gasification is moving beyond technical feasibility toward commercial viability as feedstock logistics, offtake frameworks, policy stacking, carbon-intensity monetization, and credit-trading mechanisms mature. To learn more about investable emerging opportunities in the next generation of low-carbon fuels across feedstocks (MSW, wood) and end-use pathways (hydrogen, Fischer–Tropsch liquids, and beyond)—including detailed cost-of-production models, carbon-intensity benchmarks, and region-specific project economics—consult FGE NexantECA’s Biorenewables Insight: Biomass Gasification report.

By turning waste into value and policy into profit, biomass gasification closes the carbon loop—bringing circularity to a system built on extraction—reminding us that the future of carbon lies not just in extracting more, but also in using what we already have more wisely.

Author...

Luke Downing, Senior Analyst

About Us - FGE NexantECA is the leading advisor to the energy, refining, and chemical industries. Our clientele ranges from major oil and chemical companies, governments, investors, and financial institutions to regulators, development agencies, and law firms. Using a combination of business and technical expertise, with deep and broad understanding of markets, technologies, and economics, FGE NexantECA provides solutions that our clients have relied upon for over 50 years.

Contact our team of industry experts